Welcome to Wealth Wisdom—Your Financial Edge Starts Here

Every issue of Wealth Wisdom is your go-to guide for practical insights, real-world strategies, and a dose of encouragement to help you build lasting financial confidence.

Inside, you’ll find clear tips, expert tools, and inspiring content to simplify your money decisions and move you closer to your goals—whether you’re building from scratch or ready to take things to the next level.

This is more than a newsletter—it’s your momentum.

Let’s grow stronger, smarter, and more financially free—together.

August 2025 Issue 5

August 2025 Issue 5

I wish to have future newsletters sent directly to my inbox when they become available.

Your privacy is important to us. When you share your email, we use it solely to send you helpful wellness content and updates — you can unsubscribe anytime. We will never sell or share your information with anyone, ever.

When planning for retirement, many Americans assume Social Security will be the foundation of their future income. While it's an important part of the system, Social Security was never intended to be the sole source of retirement funding. In fact, relying too heavily on these benefits could leave you financially vulnerable.

Welcome to Issue 5 of Wealth Wisdom!

🧠 "Understanding Social Security: What You Need to Know for a Stronger Retirement Plan"

🧠 "Understanding Social Security: What You Need to Know for a Stronger Retirement Plan"

Introduction

What Is Social Security?

How Does Social Security Work?

Will Social Security Still Be Around?

When Can You Claim Benefits?

How Do You Qualify for Benefits?

How Much Will You Receive?

Can You Live on Social Security Alone?

Additional Considerations

Want More Support?

Introduction

Introduction

When planning for retirement, many Americans assume Social Security will be the foundation of their future income. While it's an important part of the system, Social Security was never intended to be the sole source of retirement funding. In fact, relying too heavily on these benefits could leave you financially vulnerable.

As the landscape of retirement evolves and uncertainties around Social Security's long-term stability continue, it’s more important than ever to understand how it works, what you’re entitled to, and how it fits into a broader, more secure financial plan.

In this issue of the Wealth Wisdom Newsletter, we’ll break down everything you need to know about Social Security—from how it’s funded to when you should start claiming benefits. You’ll learn why it's critical to treat Social Security as just one piece of your retirement puzzle, and how to prepare smarter so you're not left depending on the system.

Whether you’re years away from retirement or right on the doorstep, the choices you make today can build a stronger, more confident tomorrow.

📘 What Is Social Security?

📘 What Is Social Security?

Social Security is a government-run program created in 1935 to provide financial support to retirees, disabled individuals, and survivors of deceased workers. Today, tens of millions of Americans rely on it for monthly income, with over 180 million workers contributing to the system through payroll taxes.

But here’s the key: Social Security was never meant to be your entire retirement income. It was designed to supplement—just a piece of the puzzle, not the whole picture. Unfortunately, many Americans find themselves relying heavily on these benefits and, without them, would fall below the poverty line in retirement.

If your current plan is to let the government handle your retirement, it may be time to think again. Social Security is a support, not a solution.

Your long-term security is ultimately your responsibility.

💸 How Does Social Security Work?

💸 How Does Social Security Work?

Every time you earn a paycheck, a portion of your income is deducted to fund Social Security. This payroll tax is currently 12.4% of your income. If you work for an employer, you split that cost—6.2% from you and 6.2% from them. Self-employed? You pay the full 12.4% yourself.

But this isn’t a personal savings account. The taxes you pay today aren’t stored in a vault with your name on them. Instead, that money is used to pay current beneficiaries—the retirees, survivors, and those with disabilities who are receiving benefits now.

Roughly 85% of every dollar collected goes toward retirement and survivor benefits. The remaining 15% funds disability insurance.

It’s a pay-as-you-go system, meaning your taxes help cover today’s recipients, just as future workers’ taxes will (hopefully) help cover yours.

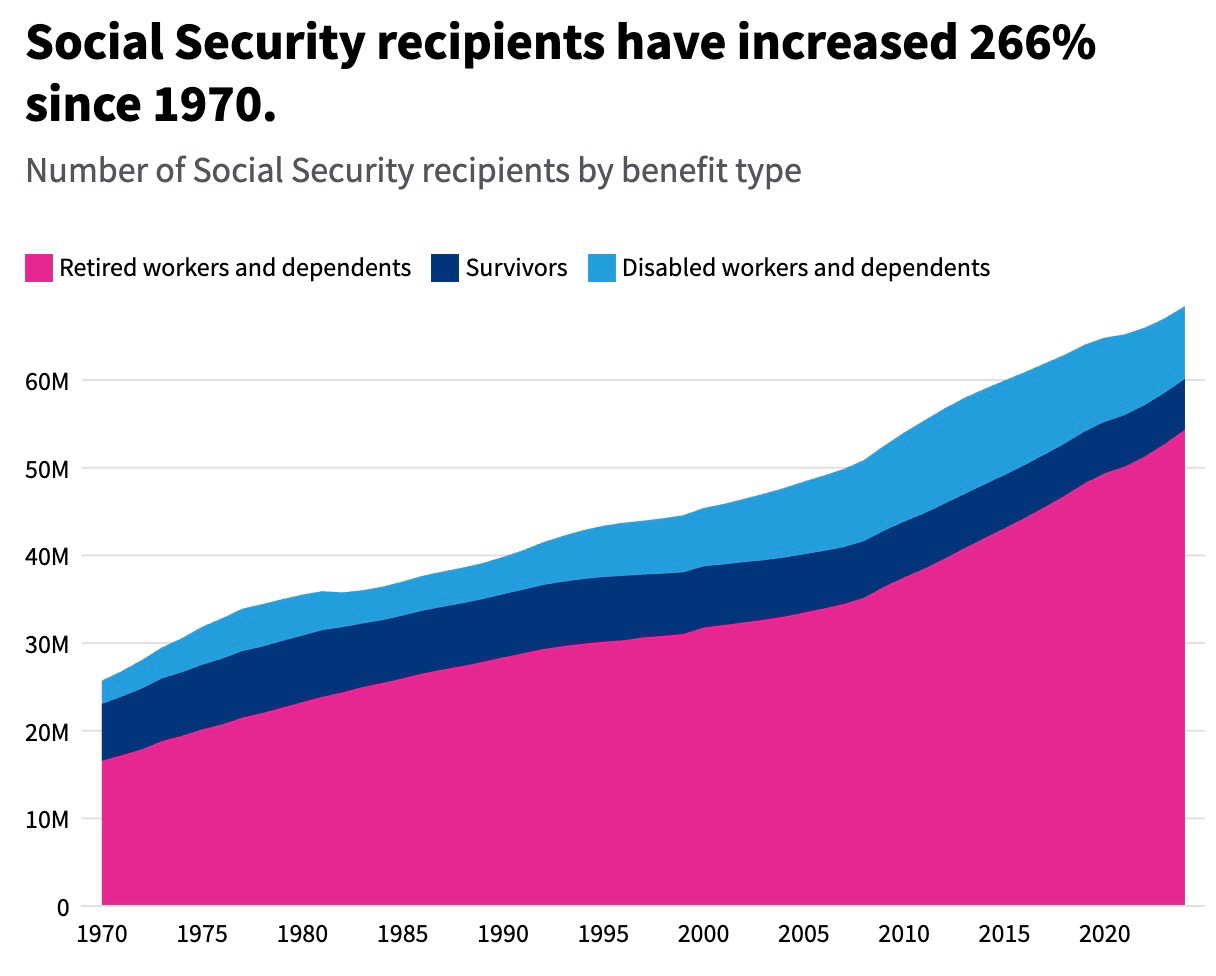

⏳ Will Social Security Still Be Around?

⏳ Will Social Security Still Be Around?

This is the million-dollar question—and the answer isn’t exactly reassuring. Social Security is currently projected to be fully funded only through 2035. After that, only about 83% of scheduled benefits will be covered unless changes are made.

What’s behind the shortfall? Demographics. Fewer workers are supporting a growing number of retirees. In 2024, roughly 2.7 workers paid into the system for each person drawing benefits. By 2035, that number will drop to 2.4. That’s a huge stress on the system.

Millions of baby boomers are reaching retirement age, and the system as it stands wasn’t built to handle this surge.

So while Social Security may not disappear, you’d be wise not to depend on it for the bulk of your retirement needs.

🕰️ When Can You Claim Benefits?

🕰️ When Can You Claim Benefits?

You can begin claiming Social Security as early as age 62. But there's a catch: the earlier you claim, the smaller your monthly benefit. The full retirement age for those born in 1960 or later is 67. Waiting until then ensures you receive 100% of your benefit.

Here’s a quick breakdown:

Waiting until age 70 maximizes your benefit, but depending on your health, financial needs, and retirement goals, claiming earlier may make more sense.

It's all about your personal circumstances and timing.

🪪 How Do You Qualify for Benefits?

🪪 How Do You Qualify for Benefits?

Before you can collect any benefits, you need to qualify. That means earning at least 40 “credits” over your working life. In 2025, you get one credit for every $1,810 earned—up to four credits per year. So, you need about 10 years of consistent work history to qualify.

This threshold is low enough that most working Americans meet it—but just remember, qualifying doesn’t guarantee a generous monthly payment.

The amount you receive depends on your earnings history and when you begin collecting.

💰 How Much Will You Receive?

💰 How Much Will You Receive?

Your Social Security benefit is based on your highest-earning 35 years of work where you paid into the system. Higher lifetime earnings mean higher monthly payments. But the formula is designed to replace a larger share of income for lower earners.

For example:

If you earned $100,000 annually, your monthly benefit may be higher, but it will replace a smaller percentage of your working income.

If you earned $40,000 annually, your benefit will be lower in dollars, but a larger portion of your income will be replaced.

Also important: the longer you wait to claim, the larger your monthly benefit (up to age 70).

It’s a balancing act between how much you get each month and how long you expect to collect.

🏡 Can You Live on Social Security Alone?

🏡 Can You Live on Social Security Alone?

In short, it would be very difficult. As of December 2024, the average Social Security check was $1,975 a month—or just under $24,000 per year. That’s barely above the poverty line for a couple.

That’s why Social Security should only be one layer of your retirement strategy. To enjoy financial independence and comfort in retirement, you’ll need other income sources: 401(k)s, IRAs, investments, or even part-time work. The sooner you begin investing, the better.

If you invest consistently and wisely during your career, you won’t have to worry about whether Social Security is enough—it’ll just be a helpful bonus.

⚖️ Additional Considerations

⚖️

✅ Can You Work and Collect Benefits?

Yes—but with restrictions. If you start collecting before full retirement age and earn more than $23,400 (2025 threshold), your benefit will be reduced by $1 for every $2 over the limit.

Once you hit full retirement age, that penalty disappears and your benefit may increase to reflect previous deductions.

✅ What About Spousal Benefits?

If you didn’t work outside the home or didn’t earn enough to qualify, you may still be eligible for spousal benefits—up to 50% of your spouse’s full benefit.

To qualify, you must be at least 62 or caring for a qualifying child. Just like personal benefits, claiming before full retirement age means a reduced amount.

✅ Will You Owe Taxes?

Maybe. Up to 85% of your benefits may be taxable if you have other income. If you file individually and your combined income exceeds $25,000—or $32,000 for joint filers—you’ll likely pay federal taxes on a portion of your Social Security income.

✅ How Do You Apply?

You can apply:

Online via the Social Security website

By calling 800-772-1213

At your local Social Security office

Have your personal info ready: birth certificate, work history, spouse details, military service records, and bank information for direct deposit.

🎯 Final Thoughts: Build a Plan That Doesn’t Depend on Social Security

🎯 Final Thoughts: Build a Plan That Doesn’t Depend on Social Security

Here’s the truth: Social Security is a nice bonus, but it should never be your primary retirement plan. The future of the system is uncertain, and even at its best, it was never designed to replace your full income.

If you’re in your 30s, 40s, or 50s, the best thing you can do is take charge of your financial future today. Contribute regularly to retirement accounts, keep your expenses in check, and stay focused on your long-term vision. The more control you take now, the less you’ll have to worry about later.

At West Egg Wealth, we’re here to walk with you every step of the way. Not with get-rich-quick advice or magic formulas—but with grounded, practical strategies that help everyday people build wealth, protect their future, and live with purpose.

📩 Want More Support?

📩 Want More Support?

Subscribe to the full West Egg Wealth newsletter series for:

✅ Actionable tips

✅ Real-life success stories

✅ Weekly encouragement

✅ Free tools and resources to build wealth and peace of mind

Or visit our community hub to access courses, connect with others, and take your next step toward financial prosperity.

Bonus Material

Bonus Material

Estate planning might not be at the top of your list of things to do, but it's an essential step in ensuring that your assets are distributed according to your wishes. Having a will is crucial, regardless of your marital status or whether you have children.

A will provides a clear, legal framework for what happens to your property after you die. Without a will, the distribution of your assets is left to the state's laws, which might not align with your intentions. In this blog, we'll explore why it's essential to have a will and the risks of dying without one.

If you’re new to West Egg Wealth, be sure to click on our Getting Started icon. There, you’ll find downloadable materials, free guides, and practical tools designed to help you build stronger financial habits and gain confidence with your money. It’s the perfect place to begin moving toward better financial health and long-term stability.

If you have any questions, thoughts, or comments you'd like to share, I'm always happy to hear from you - just send a message to info@westeggliving.com

I'm here to help!

Thank you for joining us for this edition of Wealth Wisdom! We hope you found valuable insights and encouragement as you take steps toward a stronger financial future. It’s an honor to walk alongside you as you grow in financial knowledge, confidence, and peace of mind. Remember, you’re not alone on this journey—and we’re here to support you every step of the way.

Stay tuned for next month's issue packed with more tips, insights, and motivation. Until then, be kind to yourself and keep moving forward — you’ve got this!

The content provided on this West Egg Wealth is for informational and educational purposes only and should not be considered financial, legal, or professional advice. Always consult with a qualified professional before making any changes to your personal finances. Individual results may vary and West Egg Wealth makes no guarantees regarding specific outcomes.

Use of this website and associated materials constitutes acceptance of our

I love the video on this one.

I will try dinking water every hourr like I am trying to go 250 steps each hour.. Encouraging idea.

This is great information. I love the new layout. I cannot wait for the next edition!!!

Thanks Riaan.

Great article!